.svg)

UK-India Trade: India's Economy Overview

Ejaaz Patel

As of 2025, India has become a $4 trillion economy, making it the 4th largest economy in the world. Here's a research piece on its economic make-up and drivers.

Executive Summary

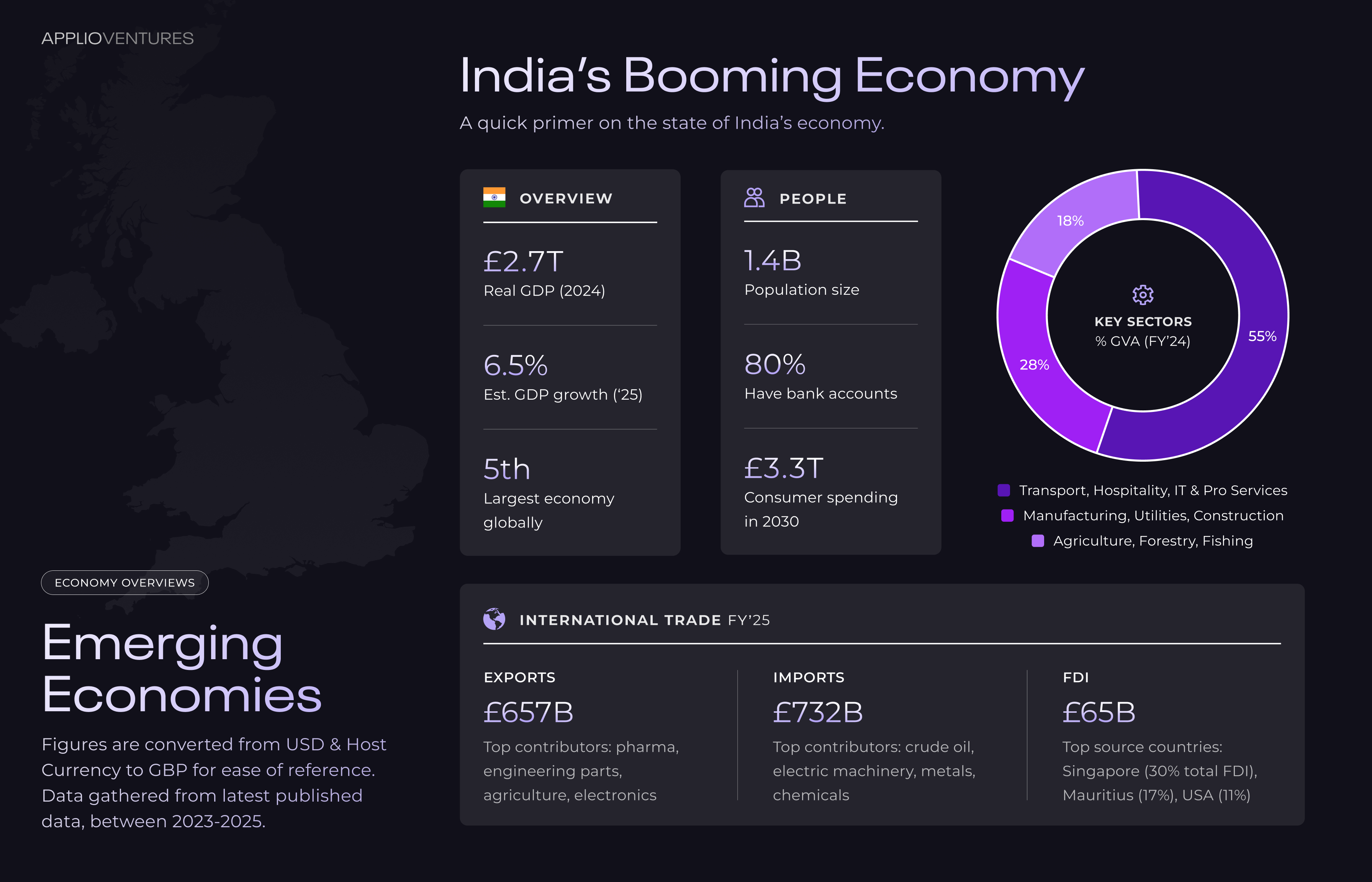

India has emerged as the world's fifth-largest economy with a £2.7 trillion real GDP, recently overtaking Japan and surpassing the UK's £2.6 trillion economy. The convergence of massive consumer market expansion - with consumer spending set to almost double by 2030 to £3.4 trillion - and robust capital market infrastructure positions India as a mature, investable market rather than an emerging opportunity. With over 500 listed companies generating £100 million-plus turnover compared to the FTSE's 375, alongside £4 trillion in stock market capitalisation versus the FTSE's £2.6 trillion, India demonstrates institutional depth that rivals developed economies. The combination of ambitious industrial policy programmes totalling over £1 trillion in infrastructure investment and a demographic dividend of 10 million yearly graduates creates unprecedented demand for professional services across consulting, legal, finance, and compliance sectors over the next five years.

Market Fundamentals

India's economic fundamentals demonstrate scale that rivals developed economies, with £2.7 trillion real GDP exceeding the UK's £2.6 trillion. The financial markets showcase institutional depth through £4 trillion in stock market capitalisation versus the FTSE's £2.6 trillion, supported by approximately £2.2 trillion in debt markets. Capital market activity reflects strong investor confidence with £23 billion in private equity deals, £34 billion in venture capital funding, and £65 billion in foreign direct investment recorded last year. Over 500 listed companies generate £100 million-plus turnover compared to 375 in the FTSE index, indicating broad corporate depth. This services-led economy maintains diversification through strong physical industries comprising over 40% of GDP.

FDI sources are diversified with Singapore leading at 30%, followed by Mauritius (17%) and the United States (11%). Trade partnerships span globally with the United States as the largest export destination ($77.5 billion), while China remains the top import partner ($101.8 billion). Key exports include mineral fuels, electrical equipment, and machinery, while major imports comprise crude petroleum, electrical machinery, and precious metals.

Infrastructure Development Drivers

India's industrial strategy targets comprehensive infrastructure modernisation through multiple coordinated programmes totalling over £1 trillion in investment. The "Make in India" initiative aims to deliver 25% of GDP from manufacturing through £20 billion in schemes across 14 sectors to boost manufacturing and exports. "Digital India" builds essential digital public infrastructure including Aadhaar for identity verification, UPI for seamless payments, and ONDC for open commerce networks. The flagship £1 trillion "Gati Shakti" scheme creates integrated infrastructure and logistics networks, incorporating 434 projects across three major economic corridors: Energy, Mineral and Cement Corridors; High Traffic Density Corridors; and Port Connectivity Corridors. Strategic technology investments include an £8 billion semiconductor mission and £3 billion for green hydrogen supporting net zero by 2070.

Major trade corridors enhance global connectivity: the India-Middle East-Europe Economic Corridor (IMEC) will integrate railway lines and port connections from India to Europe via UAE, Saudi Arabia, Jordan, and Israel, enabling smoother and faster transit of goods, while the International North-South Transport Corridor (INSTC) connects India to Russia and Central Asia through Iran. According to a 2014 study by the Federation of Freight Forwarders' Association of India, INSTC is 30% cheaper and 40% shorter in distance than traditional Suez Canal routes, reducing transit time to an average of 23 days for Europe-bound shipments compared to 45-60 days via the Suez route. Dedicated Freight Corridors including the Delhi-Mumbai Industrial Corridor create specialised rail networks optimising cargo movement and reducing transit times from 50 hours to 17 hours.

Growth Catalysts & Challenges

India's demographic trajectory drives unprecedented market expansion with consumer spending set to almost double by 2030 to £3.4 trillion, powered by middle-class growth projected to reach 60% of the population by 2047, representing approximately 1 billion people.

Educational output is substantial with 10 million graduates entering the workforce annually from an estimated 60-80 million total graduates comprising less than 5% of the population. However, significant skills gaps persist between graduate capabilities and high-skill employment requirements, with 53.5% of graduates currently occupying non-high-skill roles and half deemed "unemployable" according to the 2023-24 Economic Survey. Urbanisation accelerates from 35% to 40% by 2030, concentrating demand for professional services. Financial inclusion supports growth with over 80% of the population maintaining bank accounts and growing access to credit.

These dynamics create massive opportunities for professional services across consulting, legal, finance, and compliance sectors, particularly in workforce intermediation, skills development, and enterprise enablement solutions addressing the graduate-employment mismatch over the next five years.

A Risk Assessment

While India presents compelling investment opportunities, business leaders should acknowledge inherent operational challenges requiring strategic risk management. India's regulatory environment remains complex despite ongoing reforms, with businesses facing compliance burdens across multiple jurisdictions, evolving data privacy regulations, and sector-specific requirements that can impact operational efficiency and cost structures. Currency volatility poses additional considerations, as the Indian rupee has historically experienced fluctuations that can affect foreign exchange exposures, though recent RBI policy shifts towards market-determined exchange rates are encouraging more systematic corporate hedging practices. However, these challenges are balanced by India's demonstrated institutional maturity, systematic deregulation efforts outlined in Economic Survey 2024-25, robust capital market infrastructure, and comprehensive policy reforms designed to streamline business operations and attract sustained foreign investment across professional services sectors.

For further analysis on export-country economic research, professional services market landscapes and UK services trade, visit our Resources page.

Explore further

UK-Brazil Trade: Brazil's Economy Overview

UK-Saudi Trade: Saudi's Economy Overview

UK-India Trade: India's Economy Overview